March 26, 2025

- Inflation is a topic that occupies everyone’s thoughts; not only does it elevate your cost of living by causing fuel, grocery, transportation, and general bill prices to rise, but it also diminishes the value of the Rupee. A plate of bread-omelet that you enjoyed during your college years would likely cost you more four years after graduating. Have you ever listened to your parents reminisce about the time they watched a film in the 1960s or 70s for just ₹2 in a theater? Now, the same experience is priced at over ₹100. It’s all because of inflation! ! !

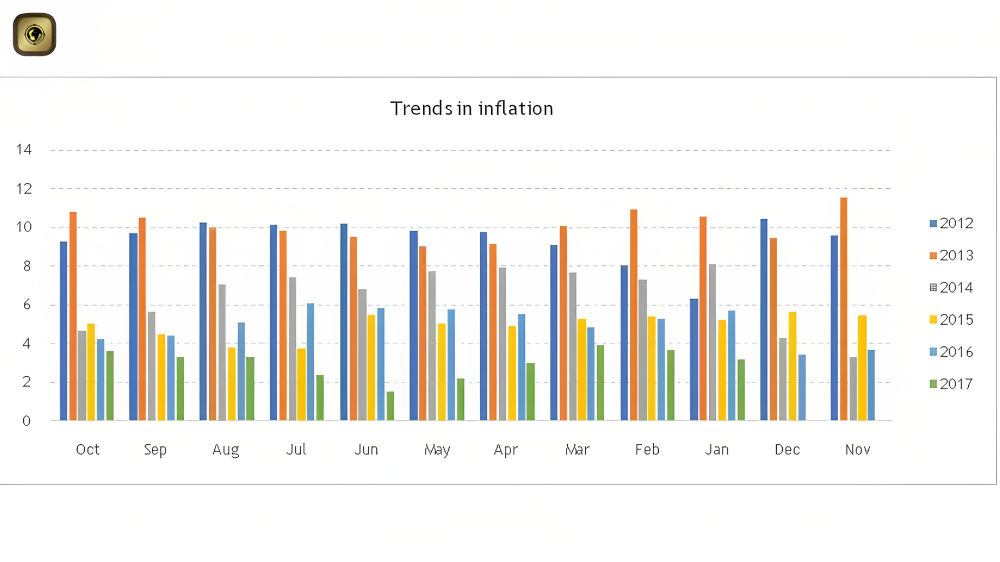

- Inflation is quantified as an annual percentage increase that is typically compared from one year to the next, meaning the inflation rate of a month is assessed against the same month from the previous year.

- According to the chart, inflation in October of this year was lower than that in October of last year (2016). In fact, inflation for each month this year has been less than that of the corresponding month last year. This indicates that the prices of goods and services in October of last year rose at a higher rate than in October of this year.

- Although its effects are felt as you make purchases of goods and utilize services, the importance of inflation in financial planning is frequently overlooked.

How many times have you compared your investment returns in relation to inflation?

- Picture this – you earn ₹100 from an investment last year as well as this year. You celebrate with a ₹20 cup of coffee. Thirty years later, that ₹100 return won’t be sufficient to buy you the celebratory cup of coffee, as it would now cost over ₹200 (assuming an average annual inflation rate of 7%).

- Apply the inflation factor to your monthly living expenses. Inflation will raise your current living costs to a significantly higher amount by the time you retire. Consequently, your retirement corpus must sustain you throughout your 2-3 decade-long retirement, reflecting the higher prices at that time.

- Neglecting to consider this ‘time value of money’, meaning the lower value of money over time, will manifest as financial difficulties during your retirement years. You may either find it hard to make ends meet, have to make compromises, or depend on family support because your retirement fund was insufficient and eventually depleted during your golden years.

- Therefore, incorporating inflation into retirement planning is vital. Here are some suggestions you might consider while planning your retirement.

- Age and expenses rise as time passes – Not only do commodity prices increase, but you also need to consider a rise in healthcare and medical expenses in your retirement planning. During your retirement years, you are likely to require and pursue more medical care and support than when you were working. Therefore, multiply your current annual medical expenses, not just by inflation, but also by a factor based on your age. Keep in mind that inflation can impact various goods differently; prices for food and fuel may vary daily, albeit with differing degrees of volatility. The costs of necessities like utilities (gas, electricity, and water) also rise consistently, contributing to the overall cost of living.

- Corpus growth outpaces inflation – Select a retirement plan that can handle increasing inflation. When selecting your retirement plan, ensure it offers an ‘increasing sum assured’ feature. This kind of protection plan will offer life coverage that increases annually to counteract the effects of inflation.

- Seek the advice of a financial expert for assistance in creating an investment portfolio that produces returns greater than inflation rates. Utilize a Future Expense Calculator to comprehend how to outpace inflation and determine how much you should save today to cover your future expenses. Contact retirement fund companies to obtain a quote and compare options to select the retirement plan that yields inflation-resistant earnings. This is essential because inflation will erode the purchasing power of your savings and consequently your retirement corpus over time.

- Pause your retirement clock – Enhanced healthcare facilities have led to an increase of over 10 years in our life expectancy within the last 20 years. From 2010 to 2014, the average life expectancy was 67. 9 years. For men, it was 66. 4 years and for women, it was 69. 6[i].

- Therefore, you need to save sufficiently to maintain your lifestyle for at least 20 years of retirement, as inflation will still exist. Consequently, you must determine when you plan to retire, how much you need to save for your retirement, and select a plan accordingly. Various types of retirement calculators are available to help you ascertain how much you need to save for insurance, how your lifestyle decisions impact your lifespan, and the amount you need to set aside to protect your family.

- In the end, an optimal retirement plan is one that offers a significant degree of diversification, is wisely allocated across debt and equity, balances the associated risks, and addresses inflation. When preparing for retirement, take inflation into account; otherwise, it could jeopardize your dreams of a comfortable retirement. Make an informed decision.

Leave A Comment